Pissing Upstream: NNPC takes a dig at Seplat-Exxon Deal?

Plus Lagos State Real Estate Transactions Law; and NAICOM Guidelines

Hello everyone. Let’s get into it.

Since the new year started, quite a lot of stuff has happened. We can’t talk about all of them today but I will try to cover as much of what has happened.

This week’s updates, quick-take:

Pissing Upstream: NNPC takes a dig at Seplat-Exxon Deal

It’s Getting Real: Lagos State Real Estate Transactions Law

NAICOM Guidelines

PISSING UPSTREAM 💦

Before we dig into this week’s top story, let’s do a quick recap here if you’re not familiar with Nigeria’s oil sector. There are three main subsectors: Upstream, Midstream, and Downstream. Our story today focuses on the Upstream sector. Learn more about these sectors in this previous thread. 👇🏽

Having cleared that up.

Sometime last month, a USD1.3 billion deal was announced between Seplat Energy Plc and Exxon Mobil Corporation (the US owner of Mobil Producing Nigeria Unlimited - MPNU). Essentially, the effect of the deal is that Exxon is selling its 100% shares in MPNU to Seplat. Appaz, the deal is one of the very first brainchild deals of Nigeria’s new Petroleum Industry Act.

The announcement of the deal has generated some reactions (supposedly) from the Nigerian National Petroleum Corporation (NNPC) - best known as a former quasi-regulator - who appears to be taking a piss at the deal. According to a media report, the NNPC is intent on claiming its interests as a holder of the Right of First Refusal (ROFR) in a JOA (joint operating agreement) with MPNU and wants to exercise that right over some of these assets covered under the Seplat-Exxon deal.

The basic gist of it is that NNPC and MNPU are parties to a JOA in respect of the operatorship of some OML assets (oil mining license - the license granted over oil wells to mine crude oil) with MPNU acting as operator. MPNU, the Exxon-owned Nigerian oil, and gas company have a percentage stake in the OML assets in Nigeria’s Upstream sector.

Usually, the way licenses over an oil well is structured may look something like this:

MPNU =========> 60%,

NNPC ==========> 30%

A few other oil companies =======> 10%.

What does this all mean?

In this instance, NNPC has a 60% stake while MPNU has a 40% stake and the JOA gives NNPC a right of first refusal over the sale of a stake by the MPNU.

What is the Right of First Refusal (preemption rights)? Imagine you just got into Lagos for NYSC, you take up an apartment with another NYSC friend of yours in Yaba. Usually, you guys would contribute money to buy common usage stuff like a fan, AC, or some other stuff. Let’s say you contributed 40% while your friend contributed 60% to buy a fan. The right of preemption basically says, if your friend were moving out of that apartment and he is not nice enough to dash you everything, he can sell his part of the 60% in the fan to you. So it will be wrong of your friend to sell the fan to another outsider and have this Lagos heat kill you.

Well, the friend in the scenario mentioned happens to be Exxon. And NNPC is feeling like a vengeful flatmate.

Things have gotten a bit tricky as Seplat argues that NNPC is misconstruing the arrangement between Seplat and Exxon. Seplat’s central argument is that the ROFR can’t be asserted on the sale and purchase of shares in a company (MPNU), and only comes into play when Seplat attempts to takeover MPNU’s participating stake/acquire MPNU’s assets under the JOA.

Assuming the object of the Seplat-Exxon deal was the sale of the OML assets under the JOA, then NNPC’s ROFR could be triggered. Considering that this is a share deal, (and not an asset sale) NNPC cannot claim a ROFR because MPNU’s 40% interest in the assets still belongs to MPNU as a company.

Two possible arguments could sway in favor of the NNPC. One, they may counter-argue that acquisition of controlling shares of the company (MPNU) holding the participating stake under the JOA effectively translates to a change in ownership of the assets. Sort of if I buy the owner of the fan, essentially I own the fan now? Another argument can only be made based on an assumption that what happened between Seplat and Exxon’s MNPU is a merger and not an acquisition of shares. In a merger situation, Seplat and Exxon become one entity, and then probably NNPC can claim its right to trigger the FROR under the JOA.

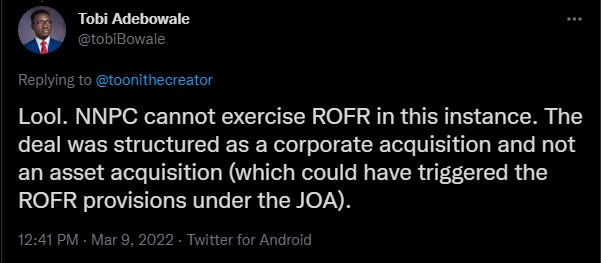

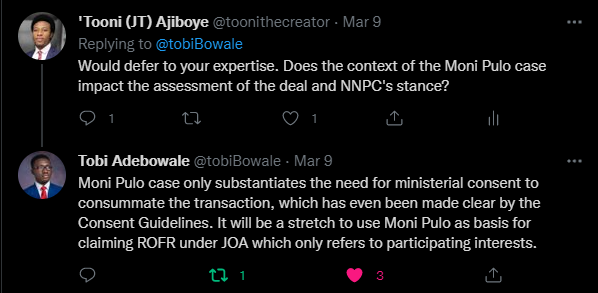

Also, this is not the first time we are seeing something like this. The share sale v. asset sale debate featured as part of the argument in a 2012 case, Moni Pulo v. Brass & Ors. In summary, that case addressed briefly the question of whether an asset sale could be equated to a corporate sale. On that, the Court said Yes. It was also clear that such a transaction, asset, or corporate sale requires the consent of the Minister of Petroleum. But that’s not our issue, in this case, I assume the Seplat-Exxon deal will follow the process of obtaining the Minister’s consent as provided for here.

Will this argument fly in the NNPC-Seplat spat? I honestly cannot say. I posted a meme on my Twitter about NNPC and its ROFR claim and this was a response from one of my ogas whom I consider an expert in the oil and gas space.

I’m inclined to agree with the view that the NNPC is merely taking a piss at the deal and it may not succeed in its bid to grab MNPU’s stake in the OML as what was disposed of in the transaction is merely the interest of shareholders in a company.

We know that NNPC cannot exercise its right over the sale of shares under the circumstances. What NNPC’s right is limited to is when such a company decides it wants to dispose of its participating stake in the OML.

Whether the NNPC succeeds in its bid of interpreting the corporate sale deal as an asset deal would probably be tested in the courts so we may expect a likely development in this direction in the coming months? Maybe.

Considering the context of tough fuel scarcity Nigerians have had to face recently, it’s befuddling that the NNPC is (in?)sincerely intent on acquiring more burden by chasing these assets, seeing how ineffective they have been in managing demand for oil across the country. But, this is Nigeria.

IT’S GETTING REAL: LAGOS STATE REAL ESTATE TRANSACTIONS LAW

Sometime last month, Lagos State passed a Real Estate Transactions Law, 2021. You can download a copy of the law here.

If your eyes have seen shege from the hands of real estate agents in Lagos while househunting, this one’s for you…

So what does the new law say?

One of the key things is the establishment of the Lagos State Real Estate Regulation Authority (LASRERA). LASRERA has some functions ranging from policy formulation to inspecting properties to ensure compliance with Lagos tenancy law, accepting and investigating petitions from the public, registering tenancy transactions and agreements above 5 years, and issuing permits to persons or organizations.

Interestingly, the law also requires the registration of “persons dealing in real estate” - quite an ambiguous description. This registration will cover individual and corporate applicants, developers, facility managers, and property management companies. Some of the registration requirements for individual applicants include the possession of a Lagos State Residents Registration Agency Number, having proper records of transactions, and maintaining a separate client account. Good luck getting that from Real Estate agents sha. In addition to this, corporate applicants also have their specific requirements for registration as provided under the law.

After registration and grant of a permit, the permit is only valid for 1 year and will be subject to annual renewal upon the payment of renewal fees stipulated by LASRERA.

Other notable developments under the law include the operational standards which indicate things like, agents not receiving money from more than one prospective client on a single property, the maximum percentage (10% & 15%) that can be charged for tenancy and sale/lease transactions respectively, having only a Legal Practitioner preparing tenancy agreements and contract documents.

In addition, the law provides for formalities in managing uncompleted/abandoned buildings, and dispute resolution. It also provides for sanctions for noncompliance with the provisions of the law: failure to register for a permit may attract a fine of 250k for individuals and 1 million for corporate organizations; failure to comply with a provision of the law may also lead to revocation of permit or fine of 100k and 10k for each day of non-compliance by a registered individual, and a fine of 500k and 25k for each day of non-compliance by a registered organization.

On the broad and possible market effect of the real estate transactions law, apart from its impact on the everyday agents that terrorize house-hunters in Lagos, I expect this law will impact the regulatory compliance playbook of most property-tech startups like KwabaNG, Spleet, Fibre, etc. To my knowledge, some of these startups have so far operated in a fairly less-regulated orbit. The requirements for registration and reporting of transactions under this new law will likely affect their operations within Lagos state as it increases the burden of compliance on them. On the brighter side, I think the fact that complaints may be made to a tribunal is a grey lining? So far, we can’t really tell how effective the implementation of these things will be.

In the meantime, get ready to report those agents that have shown you shege.

NAICOM GUIDELINES

Sometime last month, the National Insurance Commission, NAICOM, issued a new guideline titled the Insurance Web Aggregators Operational Guidelines, which aimed to regulate the conduct of web aggregators and insurance companies in Nigeria. A copy of the Guideline can be accessed here. The Guidelines have since taken effect in February 2022, however, the Guidelines also provided for a 60-day window for full compliance by existing web aggregators and insurance companies.

Before we dig into the developments under the Guidelines, I think the best way I understand the web aggregation model for insurance is as a platform/marketplace for other businesses to showcase their products. So think of it as a Jumia/Amazon for insurance companies/products, showing price comparisons, terms, and why a product may be better than the other? Something like that.

Some of the key highlights of the Guidelines include the introduction of a licensing regime for web aggregators. Asides from the basic corporate requirements (i.e., being a corporate body registered under CAC, bla bla bla) for licensing, the Guideline requires the payment of an N500,000 non-refundable application fee, an N2.5 million licensing fee, and a professional indemnity insurance cover of not less than N20 million for a company seeking to obtain the Web Aggregator license.

The license granted will be valid for an initial 2 years, and then subject to annual renewal upon payment of an annual renewal fee of N1 million. Application for renewal is to be submitted at least 45 days before the expiration of the license.

Insurance companies who are also looking to partner with, or list their products with web aggregators are required to comply with some sections of the Guidelines. Before entering into agreements with these platforms, they are required to obtain a No Objection approval from NAICOM. They must also enter into a Service Level Agreement with these platforms and the Guidelines provide some of the standard clauses which such an SLA must contain.

The Guidelines address some of the concerns that are characteristic of platform aggregation business models - anti-competitive trade practices. On this, the Guidelines stipulate that there must be transparency in transmitting customer leads to an insurer that has listed its products on its platform. Personally, I think how this will be monitored may be a little challenging though.

In the meantime, I think the introduction of the Guidelines provides a playbook for how Nigeria may be moving toward the regulation of platform-based companies. This has been a regulatory challenge for businesses that do not directly provide services but rather serve as a platform for service providers. So maybe we are witnessing the start of a trend of other forms of regulations that will spread to other sectors of the economy? We’ll see.

Editor’s Note

In next week’s Newsletter, “Sweet in the Middle(man)”, we will be talking about a planned policy change by the Federal Government in the agricultural sector.

Have an awesome week ahead!

| A guest post by

|

Many thanks! I now know a thing or two about the oil & gas sector 🙏