Lobster or Sea Pork?

How Embedded Finance Solves Access to Financial Services

Have we all had our moments at restaurants where we stare at the menu for more than a fair number of minutes and do not know what meal fits us best? Well, maybe, that's the same challenge sometimes where personal finance and financial services are concerned.

Embedded finance can be roughly explained as providing diverse financial services through easily accessible means. It could be likened to providing different financial solutions such as savings, lending, investing, and insurance to one customer in the same way a diner would offer a menu with different food options to a customer.

Why do we need embedded finance?

Throughout the history of banking and finance, the design of financial services has been averse to the concept of designing financial services that fit niche customers, unless, of course, such a customer is a high-net-worth customer. The refusal is mostly justified on the note that the risk and return trade-offs of designing personalized financial services per customer do not really make business sense. Fortunately, technology has changed this trend in the financial services sector.

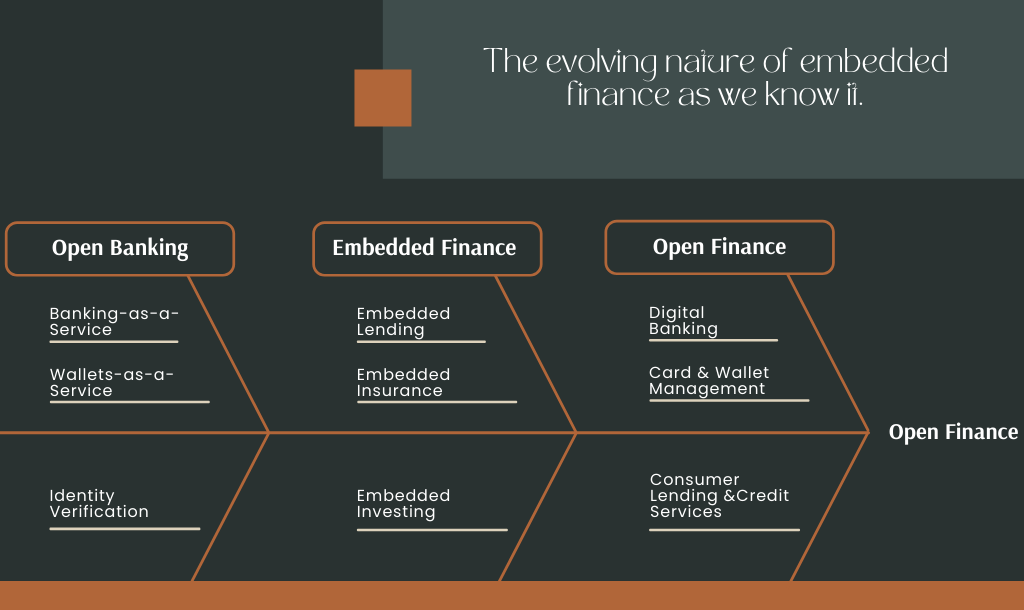

What does embedded finance look like today?

Technological solutions in the banking and finance industry have created efficient payments, data aggregation, risk assessment, and application programming interface systems that form the bedrock for embedded financing solutions.

Today, embedded financing is papering over the imperfections of a traditional financial services industry, by making sense of the financial data of millions of people and, at the click of a button allowing these customers access to diverse solutions such as faster e-commerce checkout systems, buy-now-pay-later schemes, and investment options curated to their financial appetite. In Nigeria, its use cases are currently being deployed with investment startups like Risevest, GetEquity, etc.

Caption: With Embedded Finance, every business is a potential fintech company. Source: Platformable

What are the challenges of embedded finance?

Like most revolutionary innovations, embedded financing faces its relative challenges in fitting into current market realities. One of the necessary condiments of embedded finance is access to financial data. The need for openness suggests there is a comprehensive framework that permits solutions to freely access customer financial data and use such data to responsibly curate solutions for them. Where this framework is lacking, embedded financing will look just as good as it is, on paper. Also, the challenge of the education of consumers will need to be addressed to make embedded financing more popular.

What needs to be done?

In Nigeria today, the optimal example of embedded financing would be the concept of open banking - a service that allows customers to democratize access to their financial information and data while opening those customers to a wider range of financial options including, lending and investments.

However, we are still barely at the nascent stages as embedded finance would extend into the provision of tax advisory services, and risk management, among other use cases. New initiatives like the CBN Open Banking Draft Rules are a signal that potential still lies ahead in Nigeria's experience with embedded financing.

*‘Lobster or Sea Pork?’ is an inside joke on the affordability of certain items at high-end restaurants.