Giving Credit to whom it's due

CBN Draft Credit Guarantee Guidelines; Also NITDA sanctions, the Global Standing Instruction, and a stern warning.

Loans, overdrafts and the like.

The kind of “credit” where Mr. A lends money to Mr. B for a small fee-called interest- for a particular period. Mr. B has to pay back after that period. Everybody is happy, yes? Well, mostly, unless and until Mr. B refuses to pay back the said money, and Mr. A is worried about how to cater for such a loss. Likely scenario is Mr. A is a Bank who took depositors funds in order to create a business by lending too. Dig?

This is a simplistic view to how the loan markets work in Nigeria, and pretty much anywhere. The credit model is a major way in which banks, finance houses, fintechs, moneylenders, and other regular people, use money to make money.

Now, the Nigerian market has been one which heavily depends on the loan industry and that industry has in turn been a high value market - Nigeria’s credit to private sector hits all time high.

Okay, enough of the yippy yaps.

How does this impact what we are discussing today?

We look at four regulatory policies and see how they affect the giving of credit in the Nigerian loan market, and then what happens when these credits run due?

Draft Guidelines for Credit Guarantee Companies

NITDA sanction against loan company

The Global Standing Instruction Guidelines

Stern warning to MFBs

Draft Guidelines for Credit Guarantee Companies

Earlier this month, the Central Bank of Nigeria released an Exposure Draft of Guidelines for Regulation and Supervision of Credit Guarantee Companies in Nigeria. You can access a copy of the draft regulations here.

Caveat. It’s still very much a draft, so until it is approved, it is only a picture of the direction the CBN might be heading for credit guarantees companies in Nigeria.

Why is this regulation important?

With my brief stint as a full time finance lawyer, I have sat in on credit analysis meetings and a problem that particularly stuck out in some transactions was “collateral”.

That is, if I want to lend Company A money, I need some assurance that they will repay the loan. So, I may ask Company A to provide me some sort of comfort, whether a nice high value property in Lekki, or it assigns to me a portion of the receivables it has from a contract (from any reputable company like a Shell or a Chevron), or it is guaranteed by 2 individuals who are Directors in Company A (Guarantors). In the instance of Directors, where Company A does not willingly pay back the loan, I will approach their Guarantors to pay up!

Well, not every company, especially MSMEs (small businesses with 1-500 employees, and below N500,000,000 in assets), can get a rich Director to guarantee their loans, or have properties in Lekki that will cover the loan as collateral. So in many cases, small businesses are hung out and dry - they cannot access funds to conduct more transactions, deliver goods and services, pay salaries, and generally stimulate the economy which accounts for our low GDP.

What will this new regulation do?

It is described as a bid of the CBN to create a guarantee buffer in Nigeria’s loan market, specifically for MSMEs. It creates Credit Guarantee Companies (CGCs) who will provide 3rd party credit risk mitigation for lenders - Banks, Fintechs, etc - who give out loans to small businesses.

Some of the important highlights include the permissible and non-permissible activities for CGCs. CGCs will be required to have a minimum share capital of N10,000,000,000, an initial application fee of N100,000 and a licensing fee of N1,000,000. The Guidelines also extensively provide for the expected corporate structures of CGCs in terms of required application documents, their board composition, and regulatory returns to be made, among a trove of other standard CBN regulatory requirements.

A part of the draft regulations which stand out is the Risk Management Policy where the CBN will require CGCs to maintain a framework which ensures that they prudently manage their risk concentration by sector, or borrower. Of course, this is important.

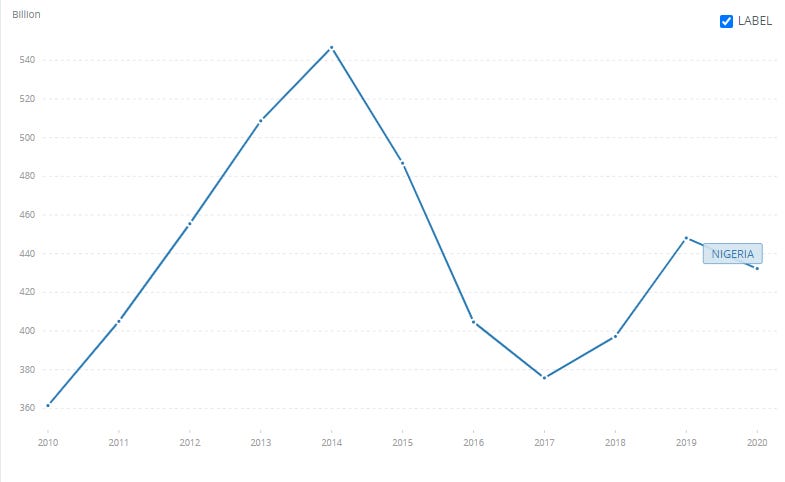

By introducing Credit Guarantee Companies, I presume the CBN is looking in the direction of promoting a solid credit market for its SMEs to access loans - which they would use to conduct more transactions, deliver goods and services, pay salaries which would improve the GDP of the Nigerian economy - which has been falling for a while now as seen below from World Bank data records.

Depending on how effecient the CGCs are, it would no doubt strengthen the position of small businesses, especially in terms of funding working capital. Evidence from other emerging markets like India & Pakistan shows that CGCs indeed do drive loan market inclusion for SMEs.

If it ever becomes a thing in Nigeria, I imagine that different SME organizations will band together to form associations, float CGCs which would then guarantee loans for member businesses. This hypothesis is based on the fact that such associations would understand better the business sense of their members as against banks and other finance institutions, for example, consider real estate practitioners’ associations.

My fear though is that this is not the first of CBN Regulations which sound like a great idea, but then don’t get market adoption - the National Collateral Registry- is an example and so far, I don’t think I’ve seen any impressive use of it in the Nigerian credit industry.

But let’s see how things go.

Overdue Credits - What Not to do

Oya soco soco!

That’s how Sokoloan danced its way into a N10 million NITDA fine. 🤧

If you do anyhow, you see anyhow. This is the vibe you get from many loan companies (I believe most of the unregulated ones) these days. So, it is usual for you to come across a strange text message reporting a conta ct on your phone for being a serial defaulter and how they will sue you and your generation for someone else’s default or beg you to warn the person to pay back their loans. See an example here.

Now, debt shaming is not a particularly strange concept. Very popular in China in fact. But we also know that there is something icky about buzzing a private individual about another person’s loan default. Most especially when they were not in the loop, maybe as a guarantor, when the transaction was agreed on.

Now, in these lenders’ supposed defence, the loan companies would say. Oh, we got the consent of the borrower to access his contacts, so we must have some leverage in sending his default notice to those contacts?

Well, that is a flawed view of how privacy laws in Nigeria work. As the NITDA sanctions show.

The Agency concluded that it found Sokoloan in breach of the:

Use of non-conforming privacy notice, contrary to Article 2.5 and 3.1(7) of the NDPR;

Insufficient lawful basis for processing personal data, contrary to Articles 2.2 and 2.3 of the NDPR;

Illegal data sharing without appropriate lawful basis, contrary to Article 2.2 of the NDPR;

From what I gleaned, NITDA argues that it also engaged the company to get it to comply with Nigeria’s data protection laws, which quite surprisingly, it failed to do. Again, most of the companies that behave like that are usually unregulated loan companies (or loan sharks, if you will).

Now. I don’t think any Nigerian law specifically says you cannot debt-shame bad debtors. However, harrassing people who are not really guarantors in a loan transaction, picks up several dimensions in the concept of the privity of contract, and processing of personal data.

The Nigeria Data Protection Regulation will bear a lot of weight on how this culture among loan companies continue in the future. The recent NITDA decision to invoke the protection is a sign that it is taking responsibility to curtail irresponsible behaviour in the data protection space.

Partner Content

Zyden Legal is an agile law firm in the business of providing world-class legal solutions to clients spread across Africa, Europe, Asia and North America.

They have expertise servicing clients across more than 48 countries, including governments, nobel peace prize winners, luxury brands, e-commerce chains, startups, and tech experts, providing much needed innovative legal solutions.

Visit their website here: https://www.zydenlegal.com/

Overdue Credits - What to do

Well, if you cannot debt-shame in peace, what other options are available where you have a bad debtor on your loan books?

Recall how I talked about some good initiatives of the CBN that are sometimes not adopted by the market? Good. One of them is the Operational Guidelines on the Global Standing Instruction.

It was released last year, effective from August 1, 2020. And it creates a system where lenders can execute a repayment instruction from any bank account of an individual borrower.

Now, it is not as simple as it sounds. The Guidelines provide for the execution of a GSI mandate by the Borrower, in favour of the Lender, and other Participating Financial Institutions.

The GSI Mandate operates simply thus: I have approached Bank A for a loan. Now Bank A knows I may not repay the loan as I promised, while still operating several bank accounts that are funded. The GSI Mandate would look something like an instruction (a signed form) from me, to all my banks, permitting them to allow Bank A debit my account to repay the loan it gave me. The mandate is effected on Nigeria’s NIBSS payments system.

Well, it so happens that most loan-giving institutions are not using the GSI, as far as I know.

Why? I frankly do not know.

But I recall having a conversation with a Risk Management Analyst, late last year who indicated that the GSI would be discouraged by banks. Nobody wants to be dealing with a pissed-off customer who had his money deducted because, get this, another bank wants to clean its bad debts books.

Regardless, I think the GSI is a solid loan repayment model that should be actively pursued by the CBN. Especially as we try to standardize the Nigerian credit market. The current options are restrictive in my opinion, leaving many lenders stranded with bad debts on their loan books.

You can find a more in-depth review of the GSI & Open Banking here.

Also, a stern warning.

On August 19, 2021, the CBN issued a Circular regarding non-permissible activities for Micro Finance Banks in Nigeria. You can find a copy of the directive here.

The directive states, among other things, that MFBs cannot handle foreign exchange transactions, should provide financial services to only retail/micro clients, are restricted to transaction limits based on their tiers, and micro credit facilities constitute a minimum of 80% of their loan portfolio.

I opined to a colleague that this reminder only indicates the direction in which the CBN may be looking at next. And of course, operators in that space such as Kuda Bank, Piggy Bank, etc have to buckle up their compliance and conduct audits to ensure they do not run afoul of CBN regulations in this regard.

That would be all for today. See you on our Quick Take Series on Friday!

Do you enjoy reading this Newsletter? Nice! I’m accepting cash donations and you can send it to me on the Abeg App: Abeg Tag @tooni https://abeg.app/

Also, don’t forget to subscribe to get weekly updates on Nigerian regulations and share with your friends and colleagues.

I enjoyed reading this article for that, I'm subscribing to your newsletters.